Monday, 10 December 2018

Monday, 10 December 2018

Dr Helen Roberts, Dr Dinithi Ranasinghe, and Professor David Lont of Otago's Department of Accountancy and Finance.

University of Otago researchers behind a study investigating corporate financial reporting techniques say shareholders need to be wary of the methods companies are increasingly using to report their results.

Co-author, Dr Helen Roberts of Otago's Department of Accountancy and Finance says the study titled Non-GAAP Disclosure and CEO Pay Levels, shines light on the association between CEO pay and unusual financial disclosure strategies.

"We found that higher levels of CEO compensation are associated with a greater likelihood of non-GAAP (Generally Accepted Accounting Principles) profit disclosure. For example, there is a 69 per cent increase in non-GAAP disclosures when we move from the median CEO cash compensation level to the upper quartile of our sample, after controlling for firm size and other factors. More simply, separating the sample into four groups by firm size, the ratio of disclosure to non-disclosure firms is consistently higher for CEOs earning above compared to CEOs earning below the median pay level within each size grouping (see Table 1). We also see an increase in the frequency of non-GAAP disclosures and an increased likelihood of non-GAAP disclosure when a CEO changes. A lack of reconciliation between GAAP and non-GAAP profits, also has a direct relationship to CEO cash compensation,” Dr Roberts says.

Table 1

| Percentage of Firms using Non GAAP Disclosures split by Size and CEO Compensation |

||

| Firm Size (market capitalisation) | CEO Cash < Median | CEO Cash ≥ Median |

| Smallest 25% of firms | 23% | 36% |

| Firms in the 25th-50th group | 37% | 48% |

| Firms in the 50th -75th group | 49% | 60% |

| Largest 25% of firms | 68% | 87% |

Co-author, Dr Dinithi Ranasinghe says the research prompts questions around the motivation for companies to use non-GAAP methods in their financial disclosures.

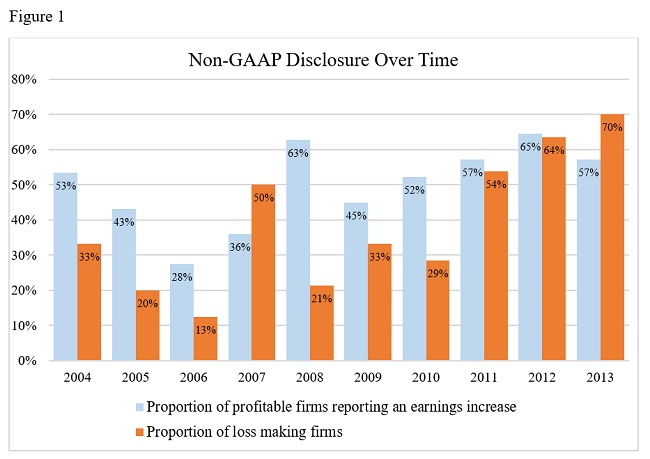

“The findings also show that managers are more likely to use these non-GAAP disclosures when their GAAP earnings benchmarks are missed. Firms experiencing a decrease in earnings demonstrate a stronger association between CEO cash compensation and the likelihood of non-GAAP disclosure. This suggests some managers may be disclosing these measures with opportunistic intentions. Looking at the trend in the use of non-GAAP measures from 2004 to 2013, firms with a loss show a greater use of non-GAAP disclosures, increasing from 33 per cent to 70 per cent, compared to a shift from 53 per cent to 57 per cent for firms reporting an earnings increase (see Figure 1).

"Put simply, when targets are missed it can be argued that managers are using non-standard reporting methods to help protect their compensation or detract from poor GAAP based earnings results,” Dr Ranasinghe says.

Professor David Lont, Head of Otago's Department of Accountancy and Finance and co-author of the study, says the practices being used should be something individual shareholders need to be wary of. “A company may argue that their use of non-GAAP measures is to explain their performance better. But if CEO's are highlighting selective profit metrics instead of GAAP measures, due to a desire to improve their compensation or disguise poorer performance – essentially painting the picture they want investors to see whilst detracting from potential negative performance shown in GAAP measures, then this should raise alarm bells,” says Professor Lont.

He adds that to ensure the picture given to shareholders is accurate, more regulation of New Zealand's reporting of non-GAAP profit figures might be needed.

The study statistically models possible factors such as firm size, governance quality, CEO turnover, CEO compensation, firm risk, and the number of analysts following the firm to understand the likelihood of these factors to explain the use of non-GAAP profit measures for New Zealand publicly listed firms during 2004 to 2013.

For more information contact:

Dr Helen Roberts

Department of Accountancy and Finance

University of Otago

Tel 03 4798072

Email helen.roberts@otago.ac.nz

Dr Dinithi Ranasinghe

Department of Accountancy and Finance

University of Otago

Tel 03 4798114

Email dinithi.ranasinghe@otago.ac.nz

Professor David Lont

Department of Accountancy and Finance

University of Otago

Tel 03 4798119

Email david.lont@otago.ac.nz

Mark Hathaway

Senior Communications Adviser

University of Otago

Mob 021 279 5016

Email mark.hathaway@otago.ac.nz

FIND an Otago Expert

Use our Media Expertise Database to find an Otago researcher for media comment.

![]()

![]()

![]()