Monday, 24 September 2018

Monday, 24 September 2018

Professor David Lont

A study jointly conducted by University of Otago and University of California researchers investigating company reporting results in the United States shows a marked increase in positive earnings surprises, determined as the difference between “street earnings” and analyst forecasts.

Street earnings make adjustment to regulated earnings, supposedly to provide a better picture of company financial performance but some question the motives behind these adjustments. Now some new research seems bound to add appreciably to these doubts.

The researchers say their study Evidence of a Positive Trend in Positive Quarterly Earnings Surprise Over the Past Two Decades, presented recently at the National Meetings of the American Accounting Association, questions whether investors are getting the straight story on companies' performance.

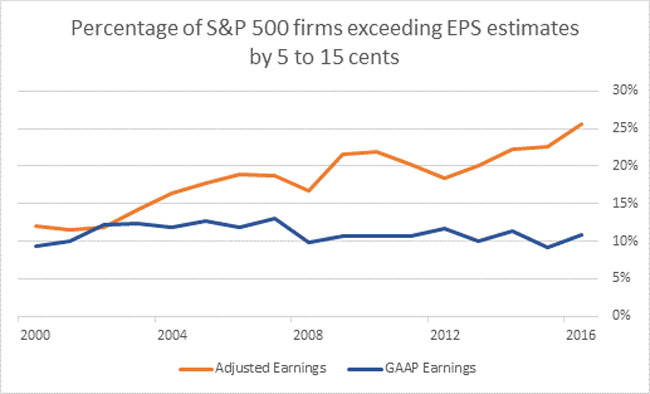

Analysing surprises in quarterly Street earnings over a 17-year period, the professors find a doubling in the proportion of reported earnings between five to 15 cents per share above analysts' forecasts for the S&P 500 – from 12.1 per cent of all earnings surprises in 2000 to 25.5 per cent in 2016.

Professor Paul Griffin

At the same time, the proportion of Street earnings reports that barely met analysts' predictions declined precipitously. Between the two periods 2000-2008 and 2009-2016, the average proportion of positive earnings surprises squeezed between zero and one cent dropped by about 15 percent and the proportion between one and two cents fell by about five percent for the S&P 500.

In marked contrast, the pattern of quarterly earnings surprises measured by Generally Accepted Accounting Principles (GAAP) was stable over the same 17 years. Among the S&P 500, GAAP earnings results five to 15 cents per share above expectations represented about 10 per cent of earnings surprises in the two years 2000-2001 and about the same percentage in 2015-2016.

While Professor David Lont, Head of the University of Otago's Department of Accountancy and Finance, and co-author Professor Paul Griffin of the University of California acknowledge that the traditional way of measuring profits – by GAAP – has been increasingly overshadowed by the use of non-GAAP metrics, their finding of a proliferation of increasingly inflated earnings surprises came as a surprise.

There are those, they write, “who might claim that so far this century the U.S. economy has experienced such an unusual period of economic growth that it has taken … analysts and investors increasingly by surprise each quarter with better-than-expected earnings performance for almost two decades.”

This view strains credulity. They warn if such a pattern continues unchallenged it could undermine the use of such forecasts.

If the pattern revealed in their study stems from earnings management, “it must be of a different form and, possibly, one more acceptable to shareholders' agents such as auditors, directors, and regulators. Non-GAAP earnings management is one such form.”

The study highlights the need for auditors and regulators to continue to monitor the use of such measures, which often show up in the notes.

The study's findings are based on an analysis of hundreds of thousands of quarterly earnings forecasts and reports involving more than 4,700 companies. While the trend toward heightened earnings surprises is seen across the entire sample, it is most pronounced for the S&P 500.

“This finding is disquieting … given their focus on strong corporate governance practices and accounting control. Apparently, S&P 500 firms are driven by a stronger need to generate positive earnings surprises than other firms,” the researchers say.

“While the study focuses on American companies, significant amounts of New Zealand investment funds are exposed to the U.S. stock market. So, any investor or fund manager needs to be aware of these findings and be cautious of any company whose trend of earnings surprises consistently heads skyward,” Professor Lont says.

“We don't want the U.S. market to experience an unnecessary shock because earnings were falsely seen as more positive than justified by the underlying performance. New Zealand's small economy and reliance on global markets makes us more vulnerable to problems in the United States than in many other countries,” Professor Lont warns.

“This type of pattern in earnings is a red flag for any investor or fund manager, because if you're seeing positive surprises all the time you need to ask 'Is this real?' At some point, the markets may say no.”

For more information, contact:

Professor David Lont

Department of Accountancy and Finance

University of Otago

Tel 03 4798119

Email david.lont@otago.ac.nz

Professor Paul Griffin

Graduate School of Management

University of California, Davis

Email pagriffin@ucdavis.edu

Mark Hathaway

Senior Communications Adviser

University of Otago

Mob 021 279 5016

Email mark.hathaway@otago.ac.nz

Electronic addresses (including email accounts, instant messaging services, or telephone accounts) published on this page are for the sole purpose of contact with the individuals concerned, in their capacity as officers, employees or students of the University of Otago, or their respective organisation. Publication of any such electronic address is not to be taken as consent to receive unsolicited commercial electronic messages by the address holder.

FIND an Otago Expert

Use our Media Expertise Database to find an Otago researcher for media comment.

![]()

![]()

![]()